The $86 Billion IPO That Named Its Own Price

SpaceX's $86 billion IPO broke down for Investment Banking interviews: the fixed price, the greenshoe math, and the aftermarket that fell.

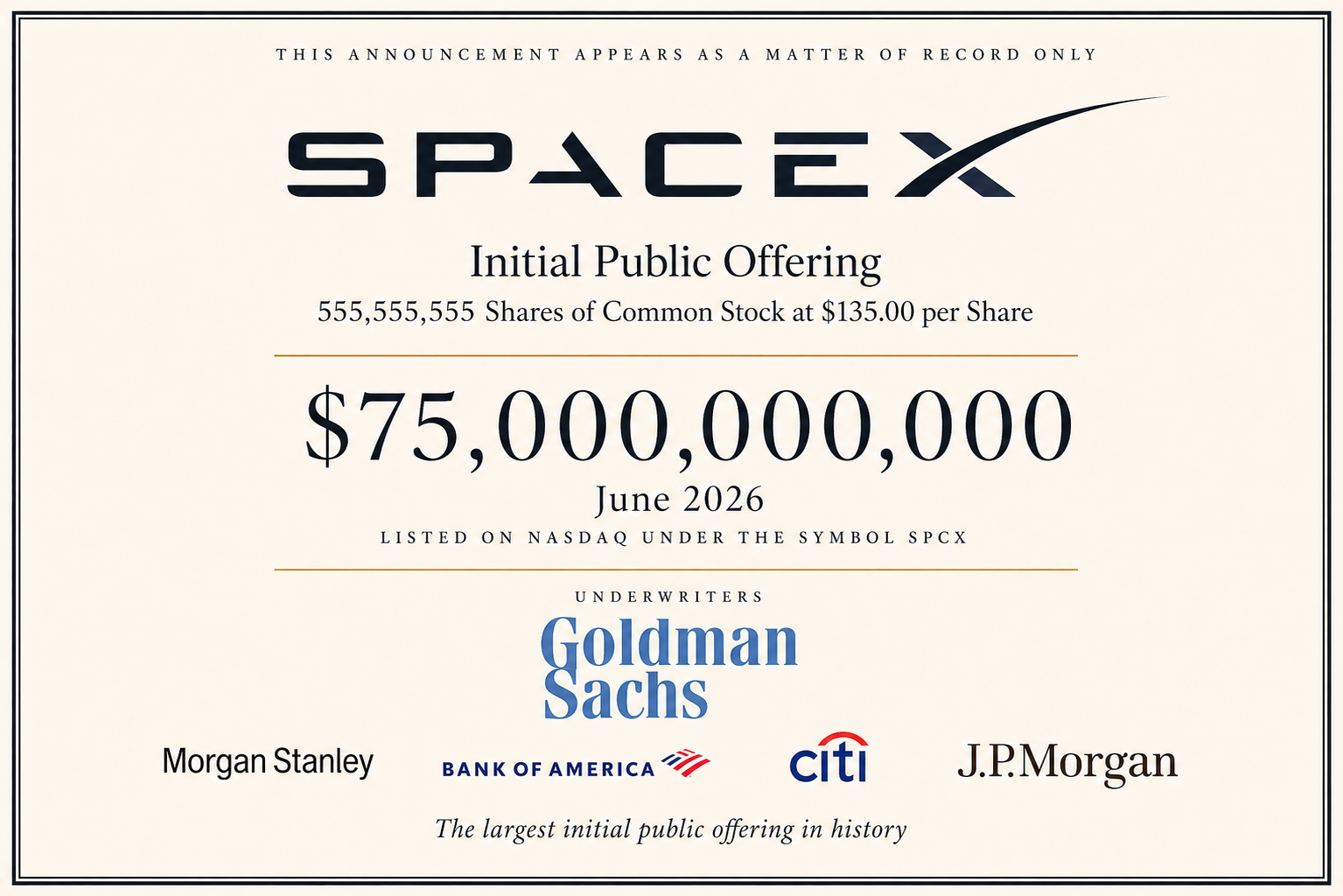

On June 12, 2026, SpaceX began trading on Nasdaq under the ticker SPCX after raising $75 billion at pricing, roughly $86 billion including the overallotment, in the largest initial public offering in history. The deal was more than triple the size of Alibaba, the previous largest US IPO.

The record is the least interesting thing about it. This deal is the best ECM case study in decades precisely because of what it skipped. No price range. No bookbuild. A retail allocation several times the norm. A founder keeping more than 80% voting control after the listing. And an aftermarket that went vertical, then fell back to earth within two weeks.

Every anomaly maps onto a mechanic candidates are expected to know cold. That makes SpaceX the deal that teaches the standard IPO process by deviation: each convention it broke is a chance to explain what the convention exists to do. This article walks the offering end to end, then closes with the section this series exists for, how to actually use the case in an interview.

Background: What SpaceX Was at Listing

The company that listed in June was not the rocket company of popular imagination. It was a three-segment conglomerate.

The financials, per the S-1 and subsequent reporting: revenue of $18,674 million in 2025, adjusted EBITDA of $6,584 million, and a GAAP net loss of nearly $5 billion, with an operating loss of $4.2 billion. The loss is the tension at the heart of the valuation, and we'll return to it.

The revenue engine is Starlink. Starlink accounted for roughly 61% of 2025 revenue at $11.4 billion, up about 50% from $7.6 billion in 2024, and had surpassed 10.3 million active customers by March 31, 2026, more than double the 4.6 million at the end of 2024. A subscription business doubling its customer base in fifteen months is the asset public investors were actually buying.

The third segment arrived four months before the listing. Musk merged SpaceX with xAI in February 2026 in a deal valuing the combined entity at $1.25 trillion, making AI infrastructure a core part of the story. The related-party tangle deserves a flag in any interview discussion: Tesla owns 18.99 million SpaceX shares, worth about $2.56 billion at the IPO price, and xAI purchased $269 million of Tesla Megapacks in April. Public investors bought into a web of Musk-entity transactions, disclosed but structurally unusual.

The competitive context also matters. Anthropic confidentially filed its IPO prospectus the same week, and OpenAI was preparing to file in the coming weeks. SpaceX went first in what the market expects to be a trio of trillion-dollar-scale AI listings. Being first in that queue was itself a strategic choice: first claim on the marginal dollar of institutional AI allocation.

Why Go Public, and Why Now

Musk resisted a listing for over two decades, arguing the company's long-term ambitions were better pursued privately. Three things changed.

First, capital appetite. The merged entity's stated use of proceeds tells the story: continued growth of AI compute infrastructure, launch facilities and vehicles, and satellite constellations. Compute buildout at frontier-AI scale plus Starship plus constellation expansion is a capital program that outruns even SpaceX's private fundraising machine of tender offers and venture rounds.

Second, the window. As covered in our June Markets Debrief, H1 2026 equity issuance set records, with US IPO and secondary sales topping $250 billion in the half, and Alphabet raising nearly $85 billion in a landmark offering. Issuers sell when valuations are defensible and demand is deep. Both held in June, despite a hawkish Fed, because equity windows key off earnings confidence and volatility rather than the level of the base rate.

Third, the race. Going public before Anthropic and OpenAI meant pricing into an index-flow and allocation environment those listings will crowd.

One thread to label carefully: reporting indicated Musk had discussed with colleagues the possibility of eventually combining SpaceX with Tesla. That is speculation about intent, not a disclosed plan. In an interview, cite it as chatter if at all, never as fact.

The Offering Structure: Four Broken Conventions

The spine of the case. Each anomaly, taught against the standard it replaced.

The fixed price

The standard process: file with a price range, run a one-to-two-week roadshow, build a book of institutional demand, then price based on where the book clears. The bookbuild exists for price discovery (mapping the demand curve), for allocation leverage (rewarding long-term holders over flippers), and for de-risking (the syndicate learns whether the deal works before anyone commits).

SpaceX skipped all of it. The company offered a take-it-or-leave-it price of $135, rather than providing a range and pricing off demand as is customary. It set the fixed price ahead of officially marketing the offering, after a series of testing-the-waters meetings, and told investors it would stop taking orders a day early, using the full final day to map allocations.

Why could SpaceX do this when almost no issuer can? Because price discovery is a service you need when demand is uncertain. When a brand is strong enough that the issuer credibly believes the book will cover at its chosen number, the bookbuild's main function becomes redundant, and skipping it becomes a statement of leverage: the issuer, not the syndicate, owns the price. The final count settled at 555,555,555 shares at $135, raising $75 billion. The share count alone tells you who was setting terms.

The retail allocation

Standard IPOs allocate 5–10% to retail. SpaceX wanted roughly 30% of the deal in retail hands, about $22.5 billion, distributed through platforms including Schwab, Fidelity, Robinhood, SoFi, and E*Trade, plus a direct share program reserving up to 5% for certain employees and persons.

Why issuers usually don't: retail paper is flighty, allocation is operationally messy, and institutions provide the stable base a new listing wants. Why SpaceX did: a founder with a retail following this large converts customers and fans into shareholders, builds a political constituency of millions of holders, and, cynically or not, distributes the first-day pop to the crowd rather than to hedge funds. A dedicated roadshow event for around 1,500 retail investors made the strategy explicit.

The control structure

Musk retained over 82% voting control after the offering. Public shareholders bought economic exposure with essentially no governance rights. The interview-relevant mechanics: super-voting structures typically trade at a governance discount, they complicate index eligibility (S&P has restricted new multi-class entrants since 2017), and they mean the usual public-market discipline (activists, proxy contests, hostile interest) simply does not apply. Whoever bought SPCX bought Musk's judgment, unhedged.

The greenshoe, done conventionally

The one piece of the deal that followed the textbook, which makes it the cleanest place to teach the textbook. The underwriters held an option to purchase an additional 83.33 million shares at the IPO price, worth $11.2 billion. Run the arithmetic: 83.33 million against a base of 555.56 million is almost exactly 15%, the standard overallotment convention.

What a greenshoe does: the syndicate sells 115% of the base deal at pricing, going short 15%. If the stock trades down, they buy shares in the market to cover, supporting the price (stabilization). If the stock trades up, they exercise the option and cover at the IPO price instead. It's a price-support mechanism that costs the issuer nothing unless the deal works, in which case the issuer sells more stock.

One derived inference, flagged as such: the $75 billion base plus the $11.2 billion option matches the roughly $86 billion headline figure attached to the debut, which implies the greenshoe was exercised in full. Given where the stock traded (next section), full exercise is exactly what the mechanics predict.

The Valuation Question

The anticipated market cap at pricing was $1.77 trillion, against $18.7 billion of revenue and an operating loss. That is roughly 95x trailing sales. The comparison that circulated during the roadshow: among the nine public trillion-dollar companies, the smallest by revenue was Micron at $58 billion, and the least profitable was Tesla at $3.8 billion of 2025 net income. SpaceX listed with a third of the revenue of the smallest member of the club and negative earnings.

How would you actually value it in an interview? Sum-of-parts is the only defensible frame. Starlink is a subscription business at $11.4 billion of revenue growing 50%, so it takes a premium recurring-revenue multiple; the launch business is a contracts-and-backlog business, valued closer to aerospace and defense comps; xAI takes whatever the market is paying for frontier AI labs, which is a number set by scarcity rather than cash flow. A DCF is nearly useless here: the cash flows are negative, the terminal assumptions would carry everything, and the honest answer is that the price was set by scarcity and narrative as much as by any model.

Two defensible views, per this series' standing format. View A: the multiple is the price of optionality on three potential category winners under one ticker, and no comparable asset exists, so comps-based objections miss the point. View B: 95x sales with a $5 billion loss is a valuation that requires flawless execution across three unrelated businesses simultaneously, and the market has priced zero probability of any of them stumbling.

The Syndicate

Goldman Sachs led the offering, followed by Morgan Stanley, Bank of America, Citigroup, and JPMorgan Chase, with approximately 125 analysts from 21 participating banks meeting management during the process. Twenty-one banks on one deal is a statement about league tables as much as distribution: a listing this size single-handedly reshapes the year's ECM rankings, and no bulge bracket could afford absence.

On fees, the honest treatment. The gross spread was not prominent in the public reporting I can verify, so what follows is market practice, labeled as such. IPO spreads compress with size the way M&A fees do: small IPOs pay the classic 7%, large deals pay 2–3%, and mega-deals compress below 1.5% (Alibaba paid roughly 1.2%; Saudi Aramco famously paid a fraction of that). Even at a heavily compressed spread, a $75–86 billion deal produces a fee pool in the high hundreds of millions, split across a 21-bank syndicate with the economics concentrated in the lead-left position. The interview point: on mega-deals, the fee percentage is small, the absolute dollars are enormous, and the league-table credit is arguably worth as much as the fee.

There's also a subtler point about what the banks were hired to do. With the price fixed by the issuer, the syndicate's traditional pricing function was gone. What remained was distribution (a $22.5 billion retail slice needs plumbing), allocation, stabilization via the greenshoe, and the analyst education machine. SpaceX effectively unbundled the IPO service stack and paid for the parts it needed.

The Aftermarket: Orbit, Then Gravity

The arc, compressed: shares opened above the IPO price and surged through the first day, pushing the market value past $2 trillion. An initial surge briefly pushed SpaceX past Amazon and Microsoft in market capitalization, the stock peaked at $225.64 intraday on June 16, then fell in three consecutive sessions; by late June SPCX traded around $153, above the $135 issue price but well below the peak.

From $135 to $225.64 is a 67% gain in four sessions. From $225.64 to $153 is a 32% drawdown in the two weeks after. Both legs have mechanical explanations that matter more than the sentiment story.

The upside mechanics: index flows into a thin float. Nasdaq announced SpaceX qualified for the Nasdaq-100 as one of the fastest additions ever, with index-tracking funds set to begin buying after the July 6 close and inclusion effective July 7. Nasdaq, FTSE Russell, and other index firms agreed to fast-track inclusion, forcing passive funds to acquire shares. Meanwhile the S&P 500 declined to make an exception, and despite the $2.2 trillion market cap, the float-adjusted Russell weighting came to only 10–15 basis points. That last number is the tell: the tradable float is tiny relative to the market cap, so large index-driven fund flows can amplify short-term price swings. Forced buyers chasing a thin float is how you get 67% in four days.

The downside mechanics: the pop was flow, and flow exhausts. Once the fast money that bought for the index-inclusion trade had its move, the marginal buyer disappeared, and the stock repriced toward where fundamental holders were willing to add. The tape didn't help: the debut landed in a Nasdaq that had shed more than 7% since its June 1 all-time high, amid mounting concerns about the return on AI investment.

The line from the market commentary that will stick to this deal: SpaceX went into orbit with its IPO before crashing back to earth nearly as swiftly. Worth knowing, because your interviewer has read it too.

The Mispricing Debate, Inverted

Here is the section that earns associate-level credit, because it takes the most common IPO interview question and shows why this deal breaks it.

The standard critique of IPO pricing goes like this: banks systematically underprice deals, the first-day pop is money the issuer left on the table, and the pop exists because the syndicate's real clients are the buy-side accounts receiving allocations, not the issuer paying the fee. A 67% pop would normally be Exhibit A. At the June 16 peak, the shares sold in the offering were worth roughly $50 billion more than the issuer collected for them. On the textbook reading, that is catastrophic underpricing.

SpaceX inverts the entire argument. The banks didn't set $135. Musk did, publicly, before the roadshow, with no bookbuild for the syndicate to shade. Whatever discount existed was the issuer's deliberate choice. So the question "was the IPO mispriced?" has to be reframed, and the reframing is the answer that separates candidates.

View A: the underpricing was strategy, not error. An issuer that raised $75 billion did not need the marginal dollar; what it wanted was a successful debut, tens of millions of retail holders with gains, smooth index entry, and a stored goodwill reserve for the follow-on offerings a capital program this size will eventually require. Read this way, $135 bought exactly what it was meant to buy.

View B: the round trip to $153 shows the pop was never real value to capture. The peak was forced index buying against a thin float, not a clearing price any seller could have achieved at scale. "Money left on the table" assumes the table could have held the money; here it couldn't. On this reading the deal was priced roughly right, the pop was flow, and the drawdown was the flow unwinding.

Notice both views defend the $135 print. The trap in the room is being pushed to say "the banks blew the pricing," which is factually wrong in this deal's structure. Name who set the price and what the pop consisted of, and the trap dissolves.

How to Use This Case Study in an Interview

Which questions this case answers. "Walk me through the IPO process" (you can teach the convention and the deviation in one answer, which no other recent deal allows). "How would you value a pre-profit company" (the sum-of-parts frame above). "What does a greenshoe do" (this deal's 15% option is the worked example). "Why do IPOs pop" (the flow-versus-value decomposition). And any ECM, TMT, or aerospace coverage conversation this cycle, where not knowing this deal reads as not reading the news.

What to emphasize. The fixed-price mechanic and what a bookbuild exists to do. The 30% retail allocation against the 5–10% norm. The greenshoe arithmetic, base times 15%, and the derived full-exercise inference. The float-versus-index-flow story behind both legs of the aftermarket. These are the elements where you can demonstrate mechanism, not just recall.

What to skip in a 90-second version. The Tesla-combination chatter (speculation; mention only if asked, and label it). The xAI related-party detail (real, but a rabbit hole). The precise financial line items beyond revenue, EBITDA, and the loss.

The 60-second spoken version:

"SpaceX listed on June 12 at a fixed $135 per share, raising $75 billion at pricing and roughly $86 billion with the greenshoe, the largest IPO ever by more than three times. The deal broke the standard playbook: no price range, no bookbuild, the issuer dictated the price, and about 30% went to retail against a typical 5–10%. It priced at roughly $1.77 trillion, about 95x trailing revenue on an operating loss, so the only defensible valuation frame is sum-of-parts across Starlink, launch, and xAI. The aftermarket is the teaching moment: the stock ran 67% to $225 on fast-tracked index inclusion into a thin float, then gave back a third of that within two weeks as the flow exhausted. The usual money-left-on-the-table critique doesn't apply here, because the discount was the issuer's choice, not the syndicate's."

The follow-ups to be ready for. "Would you have advised the fixed price?" (Answer in terms of what the bookbuild does and why this issuer uniquely didn't need it.) "What does the fall to $153 tell you?" (Flow unwinding, not thesis change; the falsifier would be a break below issue.) "How would you value Starlink standalone?" (Recurring-revenue comps, growth-adjusted; walk the subscriber math.) "What happens at lockup expiry?" (Supply event into a thin float; watch how the float-flow logic above runs in reverse.) "Was this good for the IPO market or bad for it?" (Two views: it proved the window's depth, or it absorbed the marginal dollar the next listings needed.)

Where to Drill

Deal walkthroughs are Associate-tier territory on HARDO, where the interviewer pushes past the summary into the mechanics: defend the pricing choice, decompose the pop, value the parts. An ECM deal is the variant most candidates have never rehearsed, because prep culture defaults to M&A. Running this one until the greenshoe math and the flow story are reflexive is cheap differentiation. One free Intern interview, no card, if you want to find your baseline first.

Reading is reps. Now take the rep.

Drill this in a mock- Live Deal ExamplesThe $16.5B Buyout That Left Wall Street Holding $600 Million in Losses

The $16.5B Citrix buyout, the leverage, the hung debt crisis that cost banks $600M, and the lessons for investment banking interview LBO questions.

- Live Deal ExamplesHow Microsoft Closed a $68.7B Deal Three Regulators Tried to Stop

How Microsoft closed its $68.7B Activision Blizzard deal after three regulators tried to stop it. The financing, the divestiture, the lessons for IB interviews.

- Market BriefThe Month in Question: June 2026

The Month in Question, June 2026: Warsh's first Fed hold, the SpaceX IPO record, the Iran oil shock, and how to defend a view on each in an IB interview.